To modify or foreclose? That is the lenders question!

To modify or foreclose? That is the lenders question!

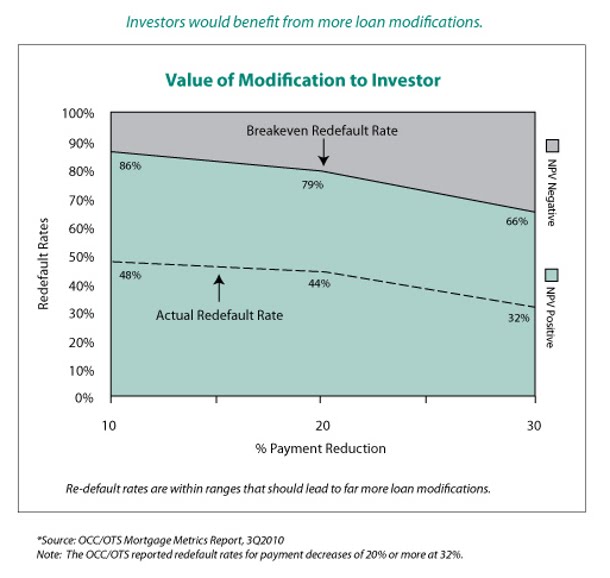

Is it better for a lender to modify or to foreclose on a delinquent borrower?

We’ve all heard the argument over whether it pays for a lender to modify the loan of an in-trouble borrower (regardless of what they are supposed to do). Does the borrower more often than not fall behind under the modified terms and re-default?

This chart from the Center for Responsible Lending shows that for the lender and for the borrower (based on a net present value analysis at various re-default rates) the modifications seem to be beneficial and should most likely be done more often.

A more detailed analysis can be found here.

{kind=link}