While interest rates have risen from depths that saw the 10-year treasury yielding 1.36% on 7/3/16, to 2.25% today, given Fed plans to tighten and pledge to shrink its balance sheet should rates be even higher?

The Fed will typically engage in the monetary policy of tightening and lift the Fed Funds rate when the two key components of its mandate, full employment and inflation at its target rate, indicate that it’s warranted to do so.

One could most definitely make the argument that with an unemployment rate of 4.3%, lowest since the 4.4% in October 2006, that employment is in good shape. And while some metrics within the employment report might suggest otherwise, this is a number that the Fed would likely consider as evidence for strong consideration of a tightening stance.

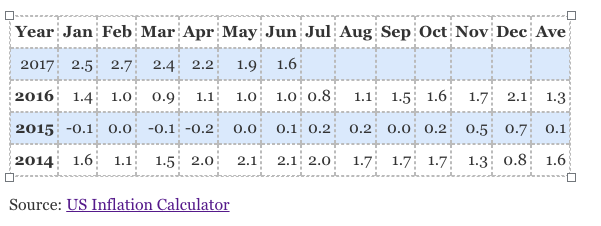

As far as the Fed’s 2% target inflation rate, whether these numbers fit the mandate is slightly less clear as the chart below shows:

But, Can The Federal Reserve Ever Really Normalize Interest Rates?

Are current treasury yield levels appropriate, or are they telling us that the ‘strength’ in the economy may not be lasting, that employment may weaken and/or that inflation may be tepid for some time to come?

Perhaps, but could there be another factor at play that may also keep the Fed from tightening to the point that interest rates become historically normalized?

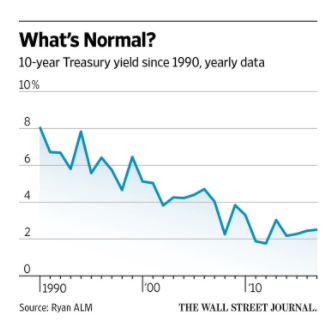

In other words, if ‘normalized’ yields for the 10-years treasury were somewhere between 4% and 6% from 1990 through the financial crisis, can the Fed reasonably ever bring them back to that level?

Or, will the term normalized interest rates come to mean something much different from what Americans have been used to?

After all, if the economy is reported to be doing so well, can’t the average American tolerate an increase from current levels?

And can the federal government reasonably manage the increased debt service that would be incurred from higher rates, given the country’s massive and ever-growing outstanding debt?

Source: Wall Street Journal and http://www.ryanalm.com/

Consider this statistic and the answer to the prior question may in fact be no!

In December 2016 the Federal Reserve raised its target for the fed funds rate by .25% to a target of 1.0% – 1.25% and, according to a TransUnion analysis, 63 million Americans holding adjustable-rate consumer debt were affected. These consumers will pay less each month when interest rates decline and pay more as they rise.

This hike that translated into an average increase in payments of $18, ‘created a challenge for 1 million consumers who were delinquent in their mortgage payment by the end of March…

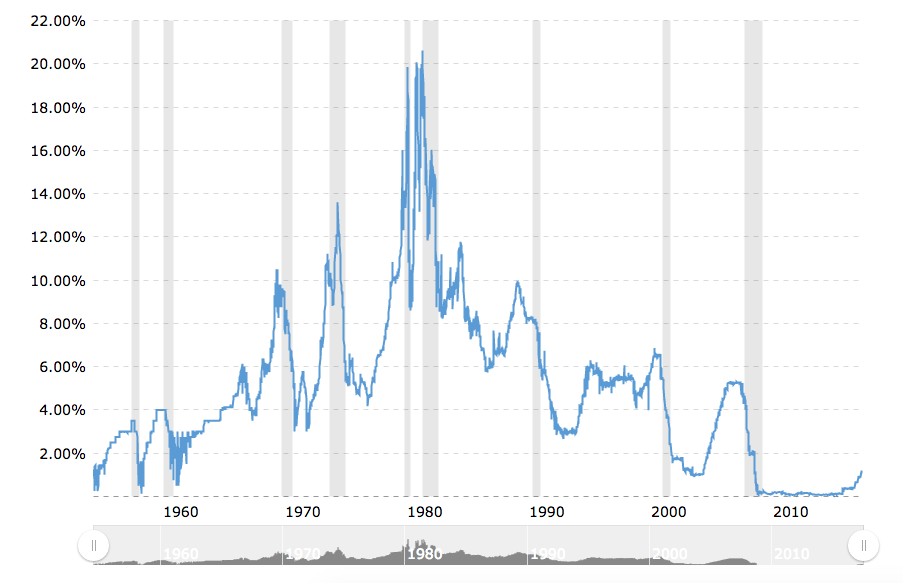

Historical Fed Funds Rate

Source: Macrotrends

…TransUnion cautioned consumers and lenders, saying while this study showed only 1 million consumers were impacted in the first quarter, it did not examine long-term impacts of a rate hike. For example, many consumers could be dipping into their savings accounts to meet the new obligations, and could eventually exhaust that source of funds.’ (Source)

So therefore, if a .25% hike and an $18 increase posed a hardship for 1,000,000 consumers, how much more of an increase can consumers tolerate?

I suppose we shall see!

__________________________________

- Who is your underwriter?

- What is the claims experience of your title insurance provider?

- Do you know whether the non-title insurance premium fees you are paying are fair and reasonable?

Pingback: U.S. Economic Strength: What Is The ‘Smart Money’ Telling us? | Hallmark Abstract LLC

Pingback: Can U.S. Interest Rates Ever Be Allowed To Rise, I Ask Again Three Years Later? | Hallmark Abstract LLC